19-03-2026 - Nadine Khodr & Alma Dizdarevic

Basel IV & The Output Floor (OF): Navigating the Future of Capital Agency

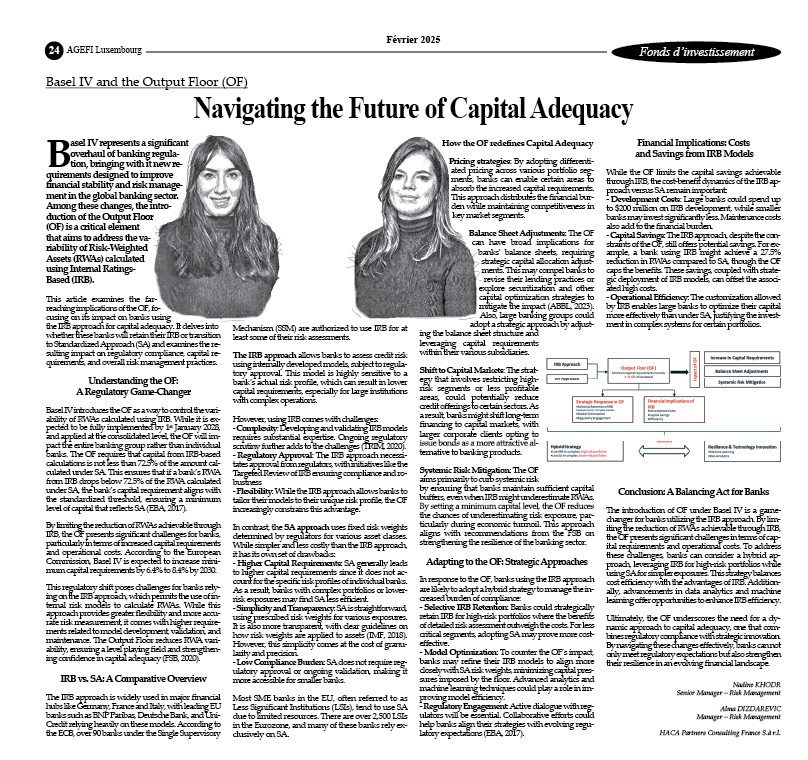

Basel IV represents a significant overhaul of banking regulation, bringing with it new requirements designed to improve financial stability and risk management in the global banking sector. Among these changes, the introduction of the Output Floor (OF) is a critical element that aims to address the variability of Risk-Weighted Assets (RWAs) calculated using Internal Ratings-Based (IRB).

This article examines the far-reaching implications of the OF, focusing on its impact on banks using the IRB approach for capital adequacy. It delves into whether these banks will retain their IRB or transition to Standardized Approach (SA) and examines the resulting impact on regulatory compliance, capital requirements, and overall risk management practices.

Understanding the OF: A Regulatory Game-Changer

Basel IV introduces the OF as a way to control the variability of RWAs calculated using IRB. While it is expected to be fully implemented by 1st January 2028, and applied at the consolidated level, the OF will impact the entire banking group rather than individual banks. The OF requires that capital from IRB-based calculations is not less than 72.5% of the amount calculated under SA. This ensures that if a bank’s RWA from IRB drops below 72.5% of the RWA calculated under SA, the bank’s capital requirement aligns with the standardized threshold, ensuring a minimum level of capital that reflects SA (EBA, 2017).

By limiting the reduction of RWAs achievable through IRB, the OF presents significant challenges for banks, particularly in terms of increased capital requirements and operational costs. According to the European Commission, Basel IV is expected to increase minimum capital requirements by 6.4% to 8.4% by 2030.

This regulatory shift poses challenges for banks relying on the IRB approach, which permits the use of internal risk models to calculate RWAs. While this approach provides greater flexibility and more accurate risk measurement, it comes with higher requirements related to model development, validation, and maintenance. The Output Floor reduces RWA variability, ensuring a level playing field and strengthening confidence in capital adequacy (FSB, 2020).

IRB vs. SA: A Comparative Overview

The IRB approach is widely used in major financial hubs like Germany, France and Italy, with leading EU banks such as BNP Paribas, Deutsche Bank, and UniCredit relying heavily on these models. According to the ECB, over 90 banks under the Single Supervisory Mechanism (SSM) are authorized to use IRB for at least some of their risk assessments.

- The IRB approach allows banks to assess credit risk using internally developed models, subject to regulatory approval. This model is highly sensitive to a bank’s actual risk profile, which can result in lower capital requirements, especially for large institutions with complex operations.

However, using IRB comes with challenges:

- Complexity: Developing and validating IRB models requires substantial expertise. Ongoing regulatory scrutiny further adds to the challenges (TRIM, 2020).

- Regulatory Approval: The IRB approach necessitates approval from regulators, with initiatives like the Targeted Review of IRB ensuring compliance and robustness

- Flexibility: While the IRB approach allows banks to tailor their models to their unique risk profile, the OF increasingly constrains this advantage.

- In contrast, the SA approach uses fixed risk weights determined by regulators for various asset classes. While simpler and less costly than the IRB approach, it has its own set of drawbacks:

- Higher Capital Requirements: SA generally leads to higher capital requirements since it does not account for the specific risk profiles of individual banks. As a result, banks with complex portfolios or lower-risk exposures may find SA less efficient.

- Simplicity and Transparency: SA is straightforward, using prescribed risk weights for various exposures. It is also more transparent, with clear guidelines on how risk weights are applied to assets (IMF, 2018). However, this simplicity comes at the cost of granularity and precision.

- Low Compliance Burden: SA does not require regulatory approval or ongoing validation, making it more accessible for smaller banks.

Most SME banks in the EU, often referred to as Less Significant Institutions (LSIs), tend to use SA due to limited resources. There are over 2,500 LSIs in the Eurozone, and many of these banks rely exclusively on SA.

How the OF redefines Capital Adequacy

- Pricing strategies : By adopting differentiated pricing across various portfolio segments, banks can enable certain areas to absorb the increased capital requirements. This approach distributes the financial burden while maintaining competitiveness in key market segments.

- Balance Sheet Adjustments : The OF can have broad implications for banks' balance sheets, requiring strategic capital allocation adjustments. This may compel banks to revise their lending practices or explore securitization and other capital optimization strategies to mitigate the impact (ABBL, 2023). Also, large banking groups could adopt a strategic approach by adjusting the balance sheet structure and leveraging capital requirements within their various subsidiaries.

- Shift to Capital Markets: The strategy that involves restricting high-risk segments or less profitable areas, could potentially reduce credit offerings to certain sectors. As a result, banks might shift long-term financing to capital markets, with larger corporate clients opting to issue bonds as a more attractive alternative to banking products.

- Systemic Risk Mitigation: The OF aims primarily to curb systemic risk by ensuring that banks maintain sufficient capital buffers, even when IRB might underestimate RWAs. By setting a minimum capital level, the OF reduces the chances of underestimating risk exposure, particularly during economic turmoil. This approach aligns with recommendations from the FSB on strengthening the resilience of the banking sector.

Adapting to the OF: Strategic Approaches

In response to the OF, banks using the IRB approach are likely to adopt a hybrid strategy to manage the increased burden of compliance:

Selective IRB Retention: Banks could strategically retain IRB for high-risk portfolios where the benefits of detailed risk assessment outweigh the costs. For less critical segments, adopting SA may prove more cost-effective.

Model Optimization: To counter the OF’s impact, banks may refine their IRB models to align more closely with SA risk weights, minimizing capital pressures imposed by the floor. Advanced analytics and machine learning techniques could play a role in improving model efficiency.

Regulatory Engagement: Active dialogue with regulators will be essential. Collaborative efforts could help banks align their strategies with evolving regulatory expectations (EBA, 2017).

Financial Implications: Costs and Savings from IRB Models

While the OF limits the capital savings achievable through IRB, the cost-benefit dynamics of the IRB approach versus SA remain important:

- Development Costs: Large banks could spend up to $200 million on IRB development, while smaller banks may invest significantly less. Maintenance costs also add to the financial burden.

- Capital Savings: The IRB approach, despite the constraints of the OF, still offers potential savings. For example, a bank using IRB might achieve a 27.5% reduction in RWAs compared to SA, though the OF caps the benefits. These savings, coupled with strategic deployment of IRB models, can offset the associated high costs.

- Operational Efficiency: The customization allowed by IRB enables large banks to optimize their capital more effectively than under SA, justifying the investment in complex systems for certain portfolios.

Conclusion: A Balancing Act for Banks

The introduction of OF under Basel IV is a game-changer for banks utilizing the IRB approach. By limiting the reduction of RWAs achievable through IRB, the OF presents significant challenges in terms of capital requirements and operational costs.

To address these challenges, banks can consider a hybrid approach, leveraging IRB for high-risk portfolios while using SA for simpler exposures. This strategy balances cost efficiency with the advantages of IRB. Additionally, advancements in data analytics and machine learning offer opportunities to enhance IRB efficiency.

Ultimately, the OF underscores the need for a dynamic approach to capital adequacy, one that combines regulatory compliance with strategic innovation. By navigating these changes effectively, banks can not only meet regulatory expectations but also strengthen their resilience in an evolving financial landscape.